Consignment Inventory Accounting Defined + Journal Entries %%page%%

Ocak 11, 2021

Because consignees are only tasked with selling consigned inventory, ownership remains with the consignor until it is sold to final customers. In this article, we’ll teach you consignment inventory accounting and go over the accounting process for consignors and consignee. In the realm of consignment inventory management accounting, both the supplier and the retailer are involved in tracking consignment sales. However, it’s essential to note that consigned goods are part of the supplier’s inventory exclusively. Despite the retailer being responsible for selling these goods, they do not assume ownership.

Optimise your consignment inventory control processes

In financial statements, consigned inventory is typically reported separately from owned inventory. This allows for a clear distinction between goods owned and those held on behalf of another party. Visit our accounting glossary next to learn even more about consignment inventory.

Scope of onerous contracts requirements is broader under IFRS Standards than US GAAP

For instance, a clothing manufacturer might consign its products to a department store, where the store displays and sells the items to customers. However, until a customer purchases the clothing, it remains the manufacturer’s property. You have to strike a careful balance non resident alien filed tax through turbotax when stocking the appropriate product. Customers will shop elsewhere if you do not order enough products, resulting in excess stock and storage costs. By examining historical data and trends from earlier months, you can estimate how much stock you’ll need going forward.

- While not required by accounting standards, Orange Co. transfers the goods to a consignment inventory account.

- This consignment inventory model involves the manufacturer, wholesaler, or supplier retaining ownership of the goods until the retailer successfully sells them to customers.

- Even though these goods are still owned and possessed by the consigner, it is considered good practice to create a separate account to record all the inventory movements in the company.

Consigned Inventory Accounting with Xledger

Because selling the consignment items is in everyone’s best interest, the two businesses should cooperate. Consignors, this involves assisting merchants in better comprehending your goods so that they may market them more successfully. Additionally, consignors must make sure that they communicate with suppliers whenever inquiries or problems emerge. The benefit of using consignment inventory is that you don’t have to carry the weight by yourself. Most of the time, when a retailer buys consignment inventory, they order the item in quantity and stock it at their establishment.

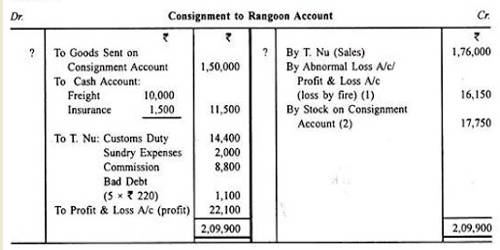

Before you consider entering a consignment inventory arrangement, you should discuss and agree on the conditions. Accounting for consignment stock includes complications that must be managed effectively to ensure accurate books. In this example, we will assume for simplicity the goods are sold for cash. The consignee pays the import duty (200) and selling expenses (300) on behalf of the consignor.

Return on Consignment Inventory

However, ownership of the inventory remains with the supplier until the products are sold to end consumers. In essence, the consignor retains control and risk over the inventory until it is purchased by the end-user. A company, Orange Co., enters into a consignment inventory agreement with another company, Red Co. Orange Co., the consignor, transfers goods worth $100,000 to Red Co., the consignee.

Unlike IAS 2, US GAAP does not contain specific guidance on storage and holding costs, which may give rise to differences from IFRS Standards in practice. Unlike IAS 2, US GAAP allows use of different cost formulas for inventory, despite having similar nature and use to the company. Therefore, each company in a group can categorize its inventory and use the cost formula best suited to it. In some cases, NRV of an item of inventory, which has been written down in one period, may subsequently increase. In such circumstances, IAS 2 requires the increase in value (i.e. the reversal), capped at the original cost, to be recognized.

This can be somewhat complex, but it’s important to understand the financial implications of such arrangements. Supply chain management is integral to running a successful business that sells products. In fact, it’s virtually impossible to succeed in the long run without appropriately managing inventory. One such inventory management strategy to consider is consigned inventory, which we’ll discuss in detail today.